Everybody Benefits from Stronger Child Care Options

Access to reliable, quality child care helps our families, workforce, employers and communities to prosper. Nebraska’s nonrefundable Child Care Tax Credit for contributors encourages taxpaying individuals or organizations to help create, expand or enhance the child care options our state needs to thrive—now, and in the years ahead.

Note: The Nebraska Department of Revenue (NDOR) reports that requests for the nonrefundable Child Care Tax Credit for now exceed the annual $2.5 million limit for contributions made in both 2026 and 2025. For more information, see NDOR's Child Care Contributor Tax Credit Authorization Table.

- Who is this tax credit for?

- What’s a nonrefundable tax credit?

- How much is the tax credit?

- How much money is available for this tax credit?

- What is a Nebraska Opportunity Zone?

- What kinds of contributions qualify for the nonrefundable tax credit?

- What other conditions apply?

- When should contributors apply for the tax credit?

-

Who is this tax credit for?

The nonrefundable Child Care Tax Credit is for taxpaying individuals and entities (such as businesses, trusts, estates, philanthropic organizations, etc.) who make qualifying contributions to help improve the availability of child care options, especially for families and communities facing serious economic challenges. To claim the credit, the contribution must be made during the calendar year corresponding to your annual state income tax return. (For example, to apply for the 2025 credit, the contribution must be made during the 2025 calendar year). To benefit from the tax credit, the contributing individual or organization must have a tax liability.

-

What’s a nonrefundable tax credit?

Nonrefundable tax credits reduce a taxpayer’s tax bill. If the amount of the credit is larger than the tax payer’s tax liability, the difference is not refunded.

In the case of the nonrefundable Child Care Tax Credit, the contributor may apply the unused amount of the credit to their tax liability for the following tax year. However, the credit must be completely used within five years of the contribution.

-

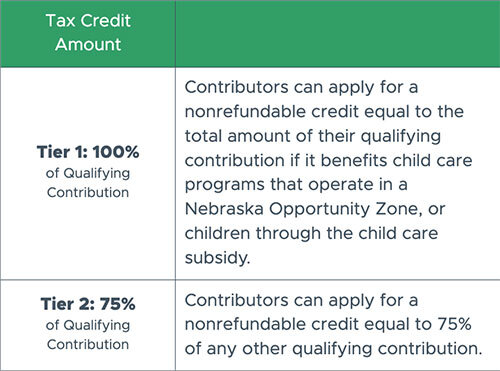

How much is the tax credit?

The nonrefundable Child Care Tax Credit is available in two tiers—either 75% or 100% of the qualifying contribution. For either tier, the total amount of the credit may not exceed $100,000 per year.

-

How much money is available for this tax credit?

The Nebraska Legislature has approved $2.5M per year for the nonrefundable Child Care Tax Credit. The Nebraska Department of Revenue (NDOR) will process applications for the credit in the order in which they are received. When the annual limit is reached, no further nonrefundable Child Care Tax Credits will be issued for contributions made in the 2025 calendar year.

Contributors can monitor how much of the annual $2.5M limit has been approved on NDOR’s website.

-

What is a Nebraska Opportunity Zone?

Nebraska Opportunity Zones are part of the federal Opportunity Zone program designed to spur investments in low-income and economically disadvantaged communities. Opportunity Zones represent specific census tracts in these communities. Nebraska currently has 44 Opportunity Zones located throughout the state in both urban and rural areas. Visit the Nebraska Department of Economic Development for more information about Opportunity Zones.

In the context of the nonrefundable Child Care Tax Credit, contributors can qualify for a 100% credit on their contribution if it benefits child care options within a designated Opportunity Zone.

-

What kinds of contributions qualify for the nonrefundable tax credit?

To qualify for the nonrefundable Child Care Tax Credit, contributions must be used by the recipient specifically for child care services. Examples of qualifying uses can include:

► Establishing, operating or expanding a child care program

► Acquisition or improvement of child care equipment or facilities

► Professional development or retention of child care program staff

► Establishing or operating a child care tuition assistance program for families in need

► Referral services that connect families to child care providersFor more detailed information about allowable uses of qualifying contributions, visit the Nebraska Department of Revenue website.

-

What other conditions apply?

► Contributions can be made by cash, cash equivalent, check, agricultural commodities or publicly traded securities. Please note that in-kind services or properties do not qualify for the tax credit.

► Contributions may be made directly to specific child care programs or indirectly through intermediary organizations or entities involved in child care initiatives.

► Contributors may only claim the credit if their contribution is made at a bona fide, arm's length basis. You may not benefit directly from the contribution. For example, a parent who pays tuition for their child at a child care program would not be able to claim their tuition payment as a "contribution."

► Contributions that are claimed as a charitable deduction on a federal income tax return are not eligible for the nonrefundable Child Care Tax Credit.

-

When should contributors apply for the tax credit?

Contributors can apply for the nonrefundable credit as soon as they have received a completed copy of the Child Care Tax Credit Contribution Receipt from the recipient of their contribution. It is not necessary to wait until the end of the tax year to apply for the credit.

How to Apply

Step 1: Document the contribution

- Obtain a completed copy of the Child Care Tax Credit Contribution Receipt from the program or entity who received your contribution. The recipient must indicate how your contribution will be used.

Step 2: Submit the tax credit application

- Use the Nebraska Department of Revenue (NDOR) website to submit your completed Child Care Tax Credit Application form and Child Care Tax Credit Contribution Receipt. You will receive an automated response verifying that your application has been received.

Step 3: Claim the tax credit

- NDOR requires at least 90 days to review tax credit applications. If your application is approved, you will receive a certification to include with your 2024 state income tax return.